Disclosure Description | References and Remarks (Unless otherwise specified, references are made to sections of the Sustainability Report 2025) |

|---|---|

(I) Governance | |

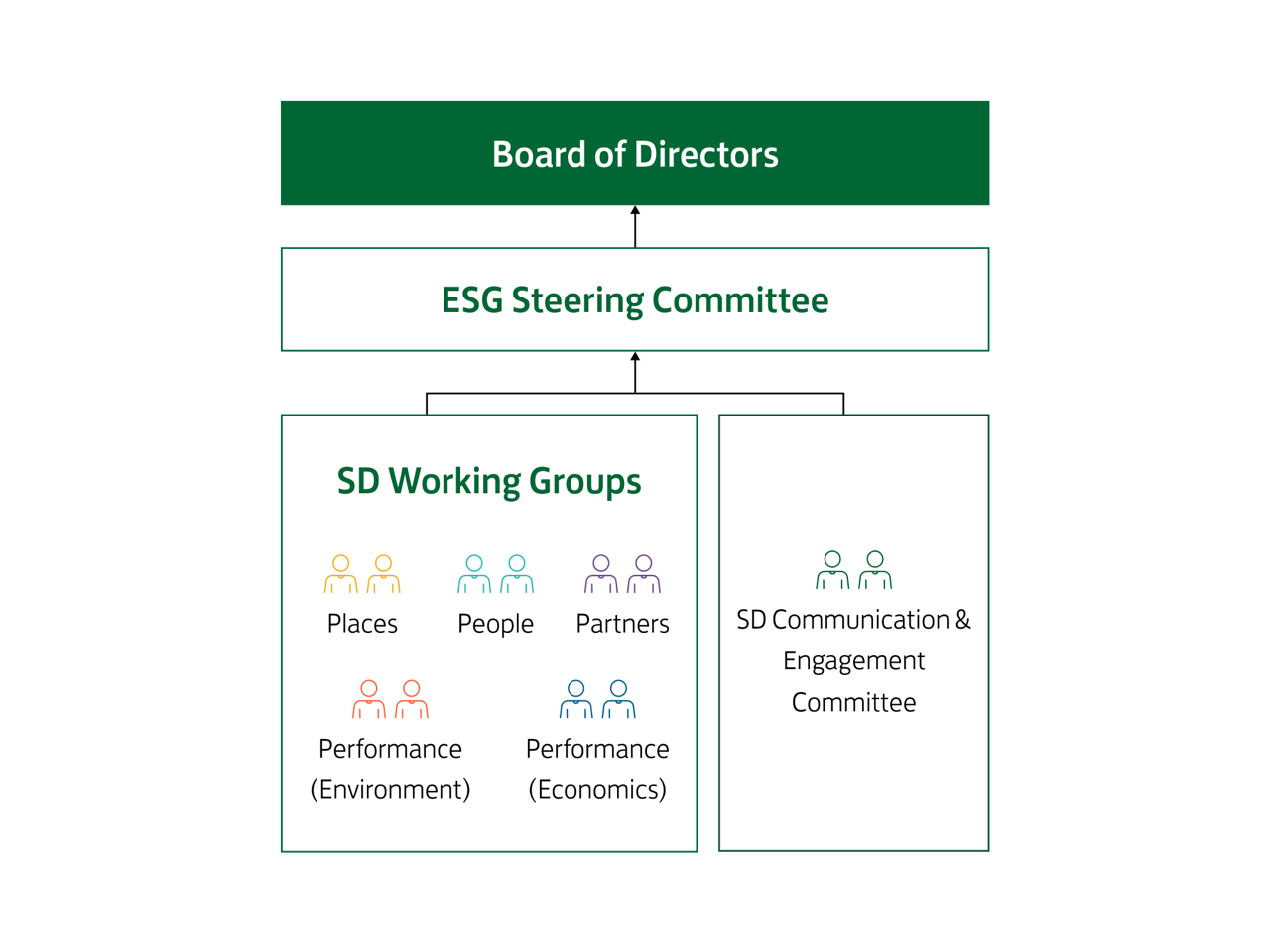

19. An issuer shall disclose information about: (a) the governance body(s) (which can include a board, committee or equivalent body charged with governance) or individual(s) responsible for oversight of climate-related risks and opportunities. Specifically, the issuer shall identify that body(s) or individual(s) and disclose information about: | SD Governance Climate- and Nature-related Financial Disclosures Performance (Economic) Annual Report 2025 – Corporate Governance Annual Report 2025 – Risk Management Corporate website – Terms of Reference for Environmental, Social and Governance Steering Committee Corporate website – Climate Change Policy |

(i) how the body(s) or individual(s) determines whether appropriate skills and competencies are available or will be developed to oversee strategies designed to respond to climate-related risks and opportunities; | Climate- and Nature-related Financial Disclosures Annual Report 2025 – Corporate Governance |

(ii) how and how often the body(s) or individual(s) is informed about climate-related risks and opportunities; | SD Governance Climate- and Nature-related Financial Disclosures |

(iii) how the body(s) or individual(s) takes into account climate-related risks and opportunities when overseeing the issuer’s strategy, its decisions on major transactions, and its risk management processes and related policies, including whether the body(s) or individual(s) has considered trade-offs associated with those risks and opportunities; | SD Governance Climate- and Nature-related Financial Disclosures Performance (Economic) |

(iv) how the body(s) or individual(s) oversees the setting of, and monitors progress towards, targets related to climate-related risks and opportunities, including whether and how related performance metrics are included in remuneration policies; and | SD Governance Performance (Environment) Climate- and Nature-related Financial Disclosures Performance (Economic) Corporate website – Terms of Reference for Environmental, Social and Governance Steering Committee Corporate website – Terms of Reference for Remuneration Committee Corporate website – Remuneration Policy |

(b) management’s role in the governance processes, controls and procedures used to monitor, manage and oversee climate-related risks and opportunities, including information about: | |

(i) whether the role is delegated to a specific management-level position or management-level committee and how oversight is exercised over that position or committee; and | SD Governance Climate- and Nature-related Financial Disclosures Performance (Economic) Annual Report 2025 – Risk Management |

(ii) whether management uses controls and procedures to support the oversight of climate-related risks and opportunities and, if so, how these controls and procedures are integrated with other internal functions. | SD Governance Climate- and Nature-related Financial Disclosures Performance (Economic) Annual Report 2025 – Risk Management |

(II) Strategy | |

Climate-related risks and opportunities 20. An issuer shall disclose information to enable an understanding of climate-related risks and opportunities that could reasonably be expected to affect the issuer’s cash flows, its access to finance or cost of capital over the short, medium or long term. Specifically, the issuer shall: | |

(a) describe climate-related risks and opportunities that could reasonably be expected to affect the issuer’s cash flows, its access to finance or cost of capital over the short, medium or long term; | Climate- and Nature-related Financial Disclosures Performance (Economic) Annual Report 2025 – Risk Management |

(b) explain, for each climate-related risk the issuer has identified, whether the issuer considers the risk to be a climate-related physical risk or climate-related transition risk; | |

(c) specify, for each climate-related risk and opportunity the issuer has identified, over which time horizons – short, medium or long term – the effects of each climate-related risk and opportunity could reasonably be expected to occur; and | |

(d) explain how the issuer defines ‘short term’, ‘medium term’ and ‘long term’ and how these definitions are linked to the planning horizons used by the issuer for strategic decision-making. | |

Business model and value chain 21. An issuer shall disclose information that enables an understanding of the current and anticipated effects of climate-related risks and opportunities on the issuer’s business model and value chain. Specifically, the issuer shall disclose: | |

(a) a description of the current and anticipated effects of climate-related risks and opportunities on the issuer’s business model and value chain; and | Partners Performance (Environment) Climate- and Nature-related Financial Disclosures Performance (Economic) |

(b) a description of where in the issuer’s business model and value chain climate-related risks and opportunities are concentrated (for example, geographical areas, facilities and types of assets). | |

Strategy and decision-making 22. An issuer shall disclose information that enables an understanding of the effects of climate-related risks and opportunities on its strategy and decision-making. Specifically, the issuer shall disclose: | |

(a) information about how the issuer has responded to, and plans to respond to, climate-related risks and opportunities in its strategy and decision-making, including how the issuer plans to achieve any climate-related targets it has set and any targets it is required to meet by law or regulation. Specifically, the issuer shall disclose information about: | |

(i) current and anticipated changes to the issuer’s business model, including its resource allocation, to address climate-related risks and opportunities; | Partners Performance (Environment) Climate- and Nature-related Financial Disclosures Performance (Economic) Annual Report 2025 – Key Business Strategies Annual Report 2025 – Risk Management |

(ii) current and anticipated adaptation and mitigation efforts (whether direct or indirect); | |

(iii) any climate-related transition plan the issuer has (including information about key assumptions used in developing its transition plan, and dependencies on which the issuer’s transition plan relies), or an appropriate negative statement where the issuer does not have a climate-related transition plan; and | SD Governance Partners Performance (Environment) Climate- and Nature-related Financial Disclosures Performance (Economic) |

(iv) how the issuer plans to achieve any climate-related targets (including any greenhouse gas emissions targets (if any)), described in accordance with paragraphs 37 to 40 of the HKEX ESG Reporting Code; and | |

(b) information about how the issuer is resourcing, and plans to resource, the activities disclosed in accordance with paragraph 22(a) of the HKEX ESG Reporting Code. | SD Governance Partners Performance (Environment) Climate- and Nature-related Financial Disclosures Performance (Economic) |

23. An issuer shall disclose information about the progress of plans disclosed in previous reporting periods in accordance with paragraph 22(a) of the HKEX ESG Reporting Code. | |

Financial position, financial performance and cash flows | |

Current financial effect 24. An issuer shall disclose qualitative and quantitative information about: | |

(a) how climate-related risks and opportunities have affected its financial position, financial performance and cash flows for the reporting period; and | Climate- and Nature-related Financial Disclosures Performance (Economic) |

(b) the climate-related risks and opportunities identified in paragraph 24(a) of the HKEX ESG Reporting Code for which there is a significant risk of a material adjustment within the next annual reporting period to the carrying amounts of assets and liabilities reported in the related financial statements. | |

Anticipated financial effect 25. The issuer shall provide qualitative and quantitative disclosures about: | |

(a) how the issuer expects its financial position to change over the short, medium and long term, given its strategy to manage climate-related risks and opportunities, taking into consideration: | |

(i) its investment and disposal plans; and | Climate- and Nature-related Financial Disclosures Performance (Economic) Annual Report 2025 – Key Business Strategies Annual Report 2025 – Management Discussion & Analysis |

(ii) its planned sources of funding to implement its strategy; and | |

(b) how the issuer expects its financial performance and cash flows to change over the short, medium and long term, given its strategy to manage climate-related risks and opportunities. | Climate- and Nature-related Financial Disclosures |

Climate resilience 26. An issuer shall disclose information that enables an understanding of the resilience of the issuer’s strategy and business model to climate-related changes, developments and uncertainties, taking into consideration the issuer’s identified climate-related risks and opportunities. An issuer shall use climate-related scenario analysis to assess its climate resilience using an approach that is commensurate with an issuer’s circumstances. In providing quantitative information, the issuer may disclose a single amount or a range. Specifically, the issuer shall disclose: | |

(a) the issuer’s assessment of its climate resilience as at the reporting date, which shall enable an understanding of: | |

(i) the implications, if any, of the issuer’s assessment for its strategy and business model, including how the issuer would need to respond to the effects identified in the climate-related scenario analysis; | Performance (Environment) Climate- and Nature-related Financial Disclosures |

(ii) the significant areas of uncertainty considered in the issuer’s assessment of its climate resilience; and | Climate- and Nature-related Financial Disclosures |

(iii) the issuer’s capacity to adjust, or adapt its strategy and business model to climate change over the short, medium or long term; | SD Governance Partners Performance (Environment) Climate- and Nature-related Financial Disclosures Annual Report 2025 – Management Discussion & Analysis |

(b) how and when the climate-related scenario analysis was carried out, including: | |

(i) information about the inputs used, including: | Climate- and Nature-related Financial Disclosures |

(1) which climate-related scenarios the issuer used for the analysis and the sources of such scenarios; | |

(2) whether the analysis included a diverse range of climate-related scenarios; | |

(3) whether the climate-related scenarios used for the analysis are associated with climate-related transition risks or climate-related physical risks; | |

(4) whether the issuer used, among its scenarios, a climate-related scenario aligned with the latest international agreement on climate change; | |

(5) why the issuer decided that its chosen climate-related scenarios are relevant to assessing its resilience to climate-related changes, developments or uncertainties; | |

(6) time horizons the issuer used in the analysis; and | |

(7) what scope of operations the issuer used in the analysis (for example, the operation, locations and business units used in the analysis); | |

(ii) the key assumptions the issuer made in the analysis; and | Performance (Environment) Climate- and Nature-related Financial Disclosures |

(iii) the reporting period in which the climate-related scenario analysis was carried out. | Climate- and Nature-related Financial Disclosures |

(III) Risk management | |

27. An issuer shall disclose information about: | |

(a) the processes and related policies it uses to identify, assess, prioritise and monitor climate-related risks, including information about: | SD Governance Climate- and Nature-related Financial Disclosures Performance (Economic) Annual Report 2025 – Risk Management |

(i) the inputs and parameters the issuer uses (for example, information about data sources and the scope of operations covered in the processes); | |

(ii) whether and how the issuer uses climate-related scenario analysis to inform its identification of climate-related risks; | |

(iii) how the issuer assesses the nature, likelihood and magnitude of the effects of those risks (for example, whether the issuer considers qualitative factors, quantitative thresholds or other criteria); | |

(iv) whether and how the issuer prioritises climate-related risks relative to other types of risks; | |

(v) how the issuer monitors climate-related risks; and | |

(vi) whether and how the issuer has changed the processes it uses compared with the previous reporting period; | |

(b) the processes the issuer uses to identify, assess, prioritise and monitor climate related opportunities (including information about whether and how the issuer uses climate-related scenario analysis to inform its identification of climate-related opportunities); and | |

(c) the extent to which, and how, the processes for identifying, assessing, prioritising and monitoring climate-related risks and opportunities are integrated into and inform the issuer’s overall risk management process. | |

(IV) Metrics and targets | |

Greenhouse gas emissions 28. An issuer shall disclose its absolute gross greenhouse gas emissions generated during the reporting period, expressed as metric tons of CO2 equivalent, classified as: | |

(a) Scope 1 greenhouse gas emissions; | Performance (Environment) ESG Reporting Standards and Principles Performance Data Summary |

(b) Scope 2 greenhouse gas emissions; and | |

(c) Scope 3 greenhouse gas emissions. | |

29. An issuer shall: | |

(a) measure its greenhouse gas emissions in accordance with the Greenhouse Gas Protocol: A Corporate Accounting and Reporting Standard (2004) unless required by a jurisdictional authority or another exchange on which the issuer is listed to use a different method for measuring greenhouse gas emissions; | Performance Data Summary |

(b) disclose the approach it uses to measure its greenhouse gas emissions including: | |

(i) the measurement approach, inputs and assumptions the issuer uses to measure its greenhouse gas emissions; | ESG Reporting Standards and Principles Performance Data Summary |

(ii) the reason why the issuer has chosen the measurement approach, inputs and assumptions it uses to measure its greenhouse gas emissions; and | |

(iii) any changes the issuer made to the measurement approach, inputs and assumptions during the reporting period and the reasons for those changes; | |

(c) for Scope 2 greenhouse gas emissions disclosed in accordance with paragraph 28(b) of the HKEX ESG Reporting Code, disclose its location-based Scope 2 greenhouse gas emissions, and provide information about any contractual instruments that is necessary to enable an understanding of the issuer’s Scope 2 greenhouse gas emissions; and | Performance (Environment) Performance Data Summary |

(d) for Scope 3 greenhouse gas emissions disclosed in accordance with paragraph 28(c) of the HKEX ESG Reporting Code, disclose the categories included within the issuer’s measure of Scope 3 greenhouse gas emissions, in accordance with the Scope 3 categories described in the Greenhouse Gas Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard (2011). | Performance (Environment) Performance Data Summary |

Climate-related transition risks 30. An issuer shall disclose the amount and percentage of assets or business activities vulnerable to climate-related transition risks. | Climate- and Nature-related Financial Disclosures |

Climate-related physical risks 31. An issuer shall disclose the amount and percentage of assets or business activities vulnerable to climate-related physical risks. | Climate- and Nature-related Financial Disclosures |

Climate-related opportunities 32. An issuer shall disclose the amount and percentage of assets or business activities aligned with climate-related opportunities. | Climate- and Nature-related Financial Disclosures |

Capital deployment 33. An issuer shall disclose the amount of capital expenditure, financing or investment deployed towards climate-related risks and opportunities. | SD Governance Climate- and Nature-related Financial Disclosures Performance (Economic) |

Internal carbon prices 34. An issuer shall disclose: | |

(a) an explanation of whether and how the issuer is applying a carbon price in decision making (for example, investment decisions, transfer pricing, and scenario analysis); and | SD Governance Climate- and Nature-related Financial Disclosures |

(b) the price of each metric tonne of greenhouse gas emissions the issuer uses to assess the costs of its greenhouse gas emissions; or an appropriate negative statement that the issuer does not apply a carbon price in decision-making. | |

Remuneration 35. An issuer shall disclose whether and how climate-related considerations are factored into remuneration policy, or an appropriate negative statement. | SD Governance Performance (Economic) Corporate website - Remuneration Policy Annual Report 2025 – Corporate Governance – Remuneration Committee |

Industry-based metrics 36. An issuer is encouraged to disclose industry-based metrics that are associated with one or more particular business models, activities or other common features that characterise participation in an industry. | See below table. |

Climate-related targets 37. An issuer shall disclose (a) the qualitative and quantitative climate-related targets the issuer has set to monitor progress towards achieving its strategic goals; and (b) any targets the issuer is required to meet by law or regulation, including any greenhouse gas emissions targets. For each target, the issuer shall disclose: | |

(a) the metric used to set the target; | Partners Performance (Environment) Climate- and Nature-related Financial Disclosures Performance (Economic) |

(b) the objective of the target (for example, mitigation, adaptation or conformance with science-based initiatives); | |

(c) the part of the issuer to which the target applies (for example, whether the target applies to the issuer in its entirety or only a part of the issuer, such as a specific business unit or geographic region); | |

(d) the period over which the target applies; | Performance Data Summary Assurance Report |

(e) the base period from which progress is measured; | |

(f) milestones or interim targets (if any); | |

(g) if the target is quantitative, whether the target is an absolute target or an intensity target; and | |

(h) how the latest international agreement on climate change, including jurisdictional commitments that arise from that agreement, has informed the target. | |

38. An issuer shall disclose information about its approach to setting and reviewing each target, and how it monitors progress against each target, including: | |

(a) whether the target and the methodology for setting the target has been validated by a third party; | Partners Performance (Environment) Climate- and Nature-related Financial Disclosures Performance (Economic) Performance Data Summary Assurance Report |

(b) the issuer’s processes for reviewing the target; | |

(c) the metrics used to monitor progress towards reaching the target; and | |

(d) any revisions to the target and an explanation for those revisions. | |

39. An issuer shall disclose information about its performance against each climate-related target and an analysis of trends or changes in the issuer’s performance. | Performance (Environment) Climate- and Nature-related Financial Disclosures Performance Data Summary Assurance Report |

40. For each greenhouse gas emissions target disclosed in accordance with paragraphs 37 to 39 of the HKEX ESG Reporting Code, an issuer shall disclose: | Performance (Environment) Climate- and Nature-related Financial Disclosures Performance Data Summary Assurance Report |

(a) which greenhouse gases are covered by the target; | |

(b) whether Scope 1, Scope 2 or Scope 3 greenhouse gas emissions are covered by the target; | |

(c) whether the target is a gross greenhouse gas emissions target or a net greenhouse gas emissions target. If the issuer discloses a net greenhouse gas emissions target, the issuer is also required to separately disclose its associated gross greenhouse gas emissions target; | |

(d) whether the target was derived using a sectoral decarbonisation approach; and | |

(e) the issuer’s planned use of carbon credits to offset greenhouse gas emissions to achieve any net greenhouse gas emissions target. In explaining its planned use of carbon credits, the issuer shall disclose: | SD Governance Performance (Environment) Climate- and Nature-related Financial Disclosures Corporate website – Climate Change Policy |

(i) the extent to which, and how, achieving any net greenhouse gas emissions target relies on the use of carbon credits; | |

(ii) which third-party scheme(s) will verify or certify the carbon credits; | |

(iii) the type of carbon credit, including whether the underlying offset will be nature-based or based on technological carbon removals, and whether the underlying offset is achieved through carbon reduction or removal; and | |

(iv) any other factors necessary to enable an understanding of the credibility and integrity of the carbon credits the issuer plans to use (for example, assumptions regarding the permanence of the carbon offset). | |

ISSB IFRS S2 Industry-based Guidance Index

Topic | Code | Metrics | References and Remarks (Unless otherwise specified, references are made to sections of the Sustainability Report 2025) |

|---|---|---|---|

Energy Management | IF-RE-130a.1 | Energy consumption data coverage as a percentage of total floor area, by property sector | ESG Reporting Standards and Principles Performance Data Summary |

IF-RE-130a.2 |

by property sector | Climate and Nature-related Financial Disclosures Performance Data Summary | |

IF-RE-130a.3 | Like-for-like percentage change in energy consumption for the portfolio area with data coverage, by property sector | Performance (Environment) – Profile of Environmental Impact | |

IF-RE-130a.4 | Percentage of eligible portfolio that

by property sector | Summary of Green Building Certification - HKGBC’s Zero-Carbon-Ready Building (ZCRB) Certification Scheme | |

IF-RE-130a.5 | Description of how building energy management considerations are integrated into property investment analysis and operational strategy | Performance (Environment) – Climate Change Performance (Environment) – Energy | |

Water Management | IF-RE-140a.1 | Water withdrawal data coverage as a percentage of

by property sector | ESG Reporting Standards and Principles Performance Data Summary |

IF-RE-140a.2 |

by property sector | Climate and Nature-related Financial Disclosures Performance Data Summary | |

IF-RE-140a.3 | Like-for-like percentage change in water withdrawn for portfolio area with data coverage, by property sector | Performance (Environment) – Profile of Environmental Impact | |

IF-RE-140a.4 | Description of water management risks and discussion of strategies and practices to mitigate those risks | Performance (Environment) – Water Climate and Nature-related Financial Disclosures | |

Management of Tenant Sustainability Impacts | IF-RE-410a.1 |

by property sector | Partners – Tenants While not structured as a cost recovery clause, we have incorporated participation in our Green Performance Pledge as a dedicated green clause in the standard tenancy agreement in Hong Kong and have developed an optional green lease addendum for tenants who are eager to include more substantial and binding language on sustainability in their tenancy agreements. |

IF-RE-410a.2 | Percentage of tenants that are separately metered or submetered for

by property sector | Partners – Tenants Performance (Environment) – Water Performance Data Summary 78% and 100% of our Green Performance Pledge participating office tenants in Hong Kong and Chinese Mainland portfolio respectively have installed energy meters. 100% of our Hong Kong and Chinese Mainland office tenants have installed water meters. | |

IF-RE-410a.3 | Discussion of approach to measuring, incentivising and improving sustainability impacts of tenants | Partners – Tenants | |

Climate Change Adaptation | IF-RE-450a.1 | Area of properties located in 100-year flood zones, by property sector | Performance (Environment) – Climate Change Climate and Nature-related Financial Disclosures |

IF-RE-450a.2 | Description of climate change risk exposure analysis, degree of systematic portfolio exposure, and strategies for mitigating risks | Performance (Environment) – Climate Change Climate and Nature-related Financial Disclosures | |

Activity | IF-RE-000.A | Number of assets, by property sector | ESG Reporting Standards and Principles Annual Report 2025 – Management Discussion & Analysis – Review of Operations – Portfolio Overview |

IF-RE-000.B | Leasable floor area, by property sector | Not disclosed. | |

IF-RE-000.C | Percentage of indirectly managed assets, by property sector | Not disclosed. | |

IF-RE-000.D | Average occupancy rate, by property sector | Annual Report 2025 – Management Discussion & Analysis – Review of Operations – Portfolio Overview |

SEE MORE IN